So this is a pretty complicated process but put simply a leveraged finance transaction takes place in the following steps:

- When the PE firm identifies the potential target, the PE firm itself creates an SPV of which it becomes the full owner (i.e. 100% shareholder).

- The PE firm collects money up and highly leverages the SPV up to a ratio of 90% debt and 10% equity. In an LBO, the interest payments on the debt are made using the cash flow generated by the acquired company. This is why a private equity firm will look for a company with a proven and successful track-record.

- The SPV receives a huge amount of cash through which it is able to purchase the target company.

- The SPV buys the target company either through a negotiation process or through a hostile process and through an IPO on the stock exchange. The aggressiveness of the operation depends on the level of debt used by the PE to buy the target company.

- The PE firm fully owns the target company.

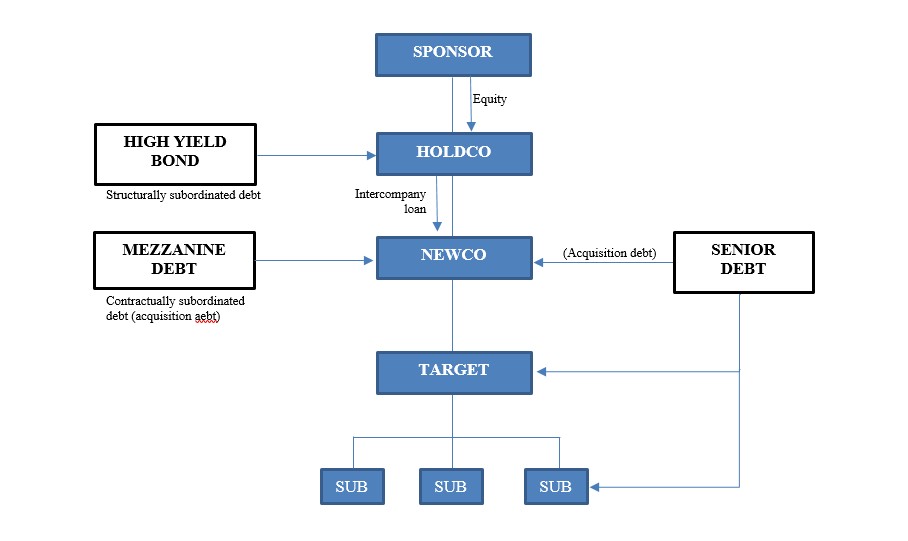

So the main job of a lawyer is to structure the deal in the most tax-efficient way possible. A new company/SPV will be set up (called Topco/Holdco) which will be owned by the PE firm. Then the acquisition vehicle will sit below this and be the SPV that purchases the shares in the target company.

The debt finance will comprise of

senior debt and

junior debt.

Senior debt comprises normally of a loan or loans from a bank which is paid back first (hence why it is called senior). Sometimes more than one bank or institutional investor is used to finance particularly large transactions and this loan called is called a

syndicated loan since the lenders are acting in a 'club'.

Junior debt, on the other hand, could comprise of things such as mezzanine debt and high yield debt which are higher risk for these lenders since they are paid back last. The debt is normally used to firstly finance the acquisition and, secondly, as working capital for the day-to-day operational and capital expenditure of the target company.

I've attached a diagram to explain and be an example of what the structure for an LBO could look like to make it easier for you.

A lawyer will first negotiate the

letter of intent then conduct

due diligence on the target company and then draft the terms of the

acquisition agreement (typically a SPA) before finally advising the firm on any

post-closing activities that need to be completed.

I think that about covers it but if you have any further questions just shoot. Here is a link to a LawCareers.Net article, written by lawyers at Weil, which explains this further.

https://www.lawcareers.net/Explore/...ndon-LLP-An-introduction-to-leveraged-buyouts

I hope this helps!

")