10 years on from the financial crisis and the European banking sector is still suffering from a painful amount of problems; the sector is too large, lacks capital and most significantly has too many unprofitable, unsustainable players – the zombie banks.

This final problem is the most troublesome and the focus of this article. The recent calamitous breakdown of the Deutsche Bank & Commerzbank merger was a timely reminder of this systemic weakness of the sector. A zombie bank is essentially a bank which is either solvent in name only, as it is only able to operate due to explicit or implicit government support, or a bank which has a ratio of Non-Performing Loans (loans where borrowers have fallen behind in their payments) high enough that they are not technically insolvent, but large enough to significantly limit their capacity to lend to new more profitable enterprises.

Both banks are prime examples of zombie banks. Commerzbank was bailed out by the German government in 2008-9 after acquiring Dresdner Bank and 15% of its shares are still held by the government. Despite the banks continued efforts to cut costs, it is earning 10-year low profits and returning a measly 4% of equity (a measure of a bank’s profitability). While Deutsche Bank was one of the few banks to survive the financial crisis without a government bailout, it is not faring any better is no better. In fact, Deutsche Bank had to rely on a $354 billion bailout from the US Federal Reserve in 2018 for fraudulent securitisation and its share price has plummeted from $76 to $8 since 2010. Furthermore, its market capitalisation (the value of the company’s shares) is the lowest it has been since the financial crisis and it has an even tinier return on equity (a measure of the bank\’s profitability) of 1%, which is 1/16th of its largest US rivals such as JP Morgan.

The merger was doomed to fail from the start as it was primarily driven by political motivations to create a national champion to rival the big US players, rather than economic viability. This came to the forefront in April when merger talks collapsed as executives realised (amongst other things) that the analysts were correct in saying that merging two zombie banks would only serve to create a larger zombie. Commerzbank’s $9.4 billion portfolio of high-risk Italian debt and the likelihood of capital requirements being imposed by the ECB were insurmountable hurdles and ultimately the merger would not create a benefit sufficient enough to offset the risk.

The Origin of The Problem – Patient 0

‘Patient 0’ of this pandemic was born out of Europe’s piecemeal response to the financial crisis (although Britain, the Netherlands and Switzerland were quick to act). The Federal Reserve in the US quickly embraced interest rate cuts, a programme of quantitative easing and a Troubled Asset Relief Programme (forcibly recapitalizing banks). However, the Eurozone did not adopt such an approach until 2013 when the sovereign debt crisis forced them to act and many European Union countries were equally poor in their response. Interest rate cuts are required in times of crisis, to incentivise investment (cost of capital is reduced), which should have a multiplier effect leading to an increase in jobs and spending.

The US’s quick response allowed the economy to recover; the assets the Fed purchased through quantitative easing included high-risk securitised loans, while the US treasury acquired underperforming loans and implemented a Trouble Asset Relief Programme, which wiped out the infection. However, this programme has largely failed in Europe, the late response has meant the economic recovery has been sluggish and inflation remains extremely low. This has forced European countries across the board to keep interest rates low to prevent a further recession. This has been recently exacerbated by the fear induced by the imminence of Brexit and the US-China trade war, leading to increasing concerns over geopolitical factors and protectionism. Indeed, in the eurozone, the ECB recently announced earlier in March this year its decision to keep interest rates at historic lows of 1.1% for the rest of the year (compared to the 2.25% rates in the US). This low interest rate policy has suppressed banks\’ profitability; this is because a bank makes money through the difference between borrowing and lending rates (known as margin).

The spread of infection

Insistence to keep these underperforming banks alive is a reflection a problem being replicated across Europe. Indeed, almost a fifth of 130 banks failed a European Central Bank stress test in 2014. In October 2016 the International Monetary Fund said European banks with more than $8 trillion in assets were still so weak they remain vulnerable.

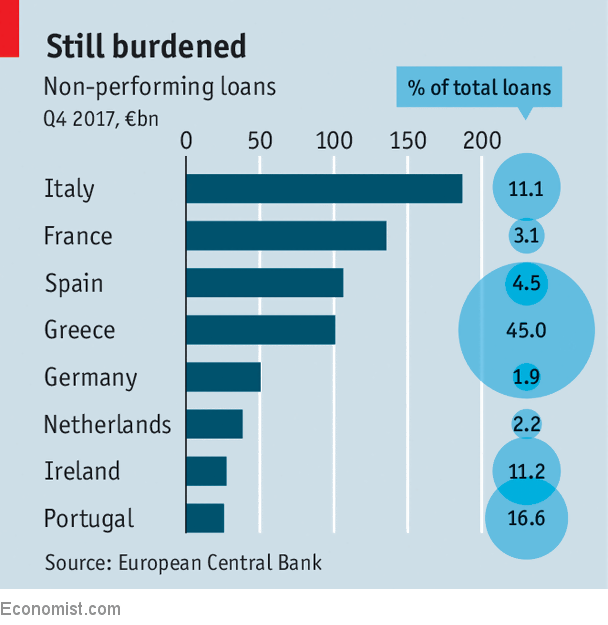

The German government alone has spent $70 billion since the financial crisis bailing out its banks and it is estimated that European banks currently hold €1 trillion of non-performing loans, which represents 30% of the banks equity, which is still higher than pre-crisis levels. Profitability is equally weak across Europe, with the average return on equity (measure of a bank’s profitability) of the 190 European Union banks being 6.5% (contrast to the US where banks such a Citigroup saw return on equity of 10%).

Italy epitomises the European zombie-bank crisis. It currently holds €100 billion of bad debt (although this has been drastically cut since 2016 where it held 360 billion), has the second largest public debt burden in Europe (Greece being the first) and has one of the highest non-performing loan ratios in the euro zone. As a result, Italian lenders have had to come to terms with the fact that most of their loans will never be repaid. For several years, shares in Italian banks have plummeted, as it became clear that they would be required to write off billions of euros’ worth of loans. Even Italy’s most prestigious lenders including the likes of Banca Monte dei Paschi di Siena—the world’s oldest bank, have been infected by a combination of poor management and financial policy and turned into zombies. Monte Paschi is now 68% owned by the government following a 5.4-billion-euro government injection in 2017 but has a return of equity of 1.23% and has seen its share depreciated in value by 70% since 2017.

Why is it problematic to allow this infection to spread?

Keeping these banks alive is problematic for several reasons:

As these banks cannot die – what incentive do they have to change the ways they operate? This is the root of the problem, as studies have shown that Zombies tend to maintain credit to companies they already have a relationship with even if they are struggling. To press for repayment would force the bank to recognise its own losses on the loans, which leaves both the banks and the companies they prop up zombified.

Managing a high proportion of NPL’s can divert resources away from more efficient and profitable business resulting in a misallocation of capital – meaning zombie banks do not positively contribute to the wider economy and keep unprofitable businesses, which are unable to grow alive.

Once burdened with NPLs, Zombies are less likely to lend capital, which in turn creates a negative feedback loop, as zombie banks slow economic growth through a misallocation of capital, which in turn increases the volume of NPL’s, diverting further resources away (Fujii and Kawai, 2010)

Parallels to the Japanese Zombie Bank Crisis

To fully appreciate the impact a zombie horde sweeping across Europe could have one need only to look at the Japanese Zombie Crisis.

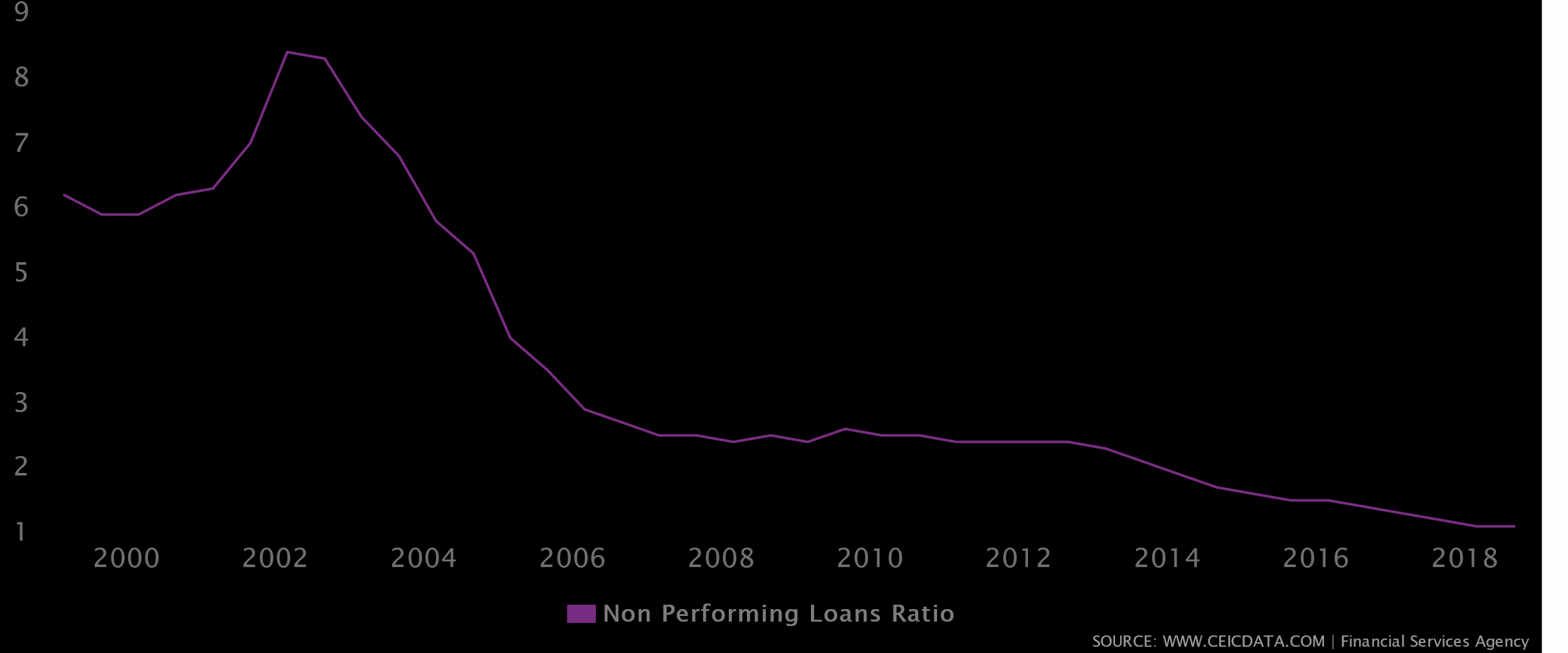

Japan in the early ’90s was suffering from the collapse of the real estate market in the 1980s, which in turn created a significant amount of NPLs and the economy began to slow. Japan just like Europe became overburdened with a high ratio of NPLs, peaking at 8% of all loans in 2001 (Italy is currently at 16%). More pressing still two of its largest urban credit co-operatives (essentially banks which lend to small borrowers and businesses) Tokyo Kyowa and Anzen were on the brink of collapse (could a similar fate be on the horizon for Commerzbank and Deutsche bank?). To counteract this the Japanese Finance Ministry undertook a policy of ‘public-private recapitalisations’, using a mixture of public and private support to recapitalise the banks.

What is recapitalisation?

This is the process of restructuring a company’s debt to equity ratio. A company which decreases its debt to equity ratio is said to have lower ‘leverage’, by issuing more shares to raise money to buy back securities. This would see the company’s earnings per share drop but would be less risky as its total debt and the amount of interest it pays to creditors is reduced. This in turn would increase the company’s liquidity leaving more money available to pay its shareholders. In the alternative a company may increase its debt to equity ratio to have higher ‘leverage’, by issuing bonds to raise money, for example. This would be useful where the share price is dropping or to defend itself from a hostile takeover, as the issue of bonds can fund the buyback of outstanding shares, which in turn should increase earnings per share. Interest payments are also tax deductible (dividends are not), so a company can also recapitalise to reduce their tax obligations.

The Bank of Japan provided a 40billion yen capital base and private banks/financial institutions provided another 40 billion in the form of low interest loans (increasing its leverage). This capital was used to create a new bank, which assumed the business of the two banks. This approach was coined ‘hougachou’ (festival of raising money from the community) and was used throughout the \’90s.

This became particularly problematic when ‘hougachou’ was adopted in the main banking sector in 1997 when Nippon Credit Bank came on the brink of collapse and the Japanese finance ministry sought to recapitalise it. A whopping 210/290 billion yen of new capital was injected from the private sector and the rest from the Bank of Japan. But despite its recapitalisation, as the bank was so large it was still under threat of insolvency. This approach was replicated across most of the banking sector and not before long the zombie horde had swept across Japan, unable to restructure, unable to take on new loans and stuck in a negative feedback loop due to their high proportion of NPLs precluding lending and in turn creating more NPLs.

The problem with ‘Hougachou’?

The fundamental problem with this approach was that it failed to address the root of the problem, the NPLs. Instead, struggling banks were reliant on other weakened private banks, which resulted in underwhelming results and only served to create a negative feedback loop.

The failure was mainly due to relying on recapitalisation alone, without any regulatory pressure or NPL resolutions, as of such there was no incentive to address the NPL problem. Regulatory pressure was evidently required, as the banks were unwilling to call in these loans as this would cause short-term loss.

This period of zombification became known as ‘Japan’s Lost Decade’ due to the fact its economy suffered from economic stagnation and price deflation with annual GDP growth of only 1.14 until 2001 (compared to its 3.89% resulting from the real estate boom in the \’80s).

Is there a cure?

Fortunately for Europe there is an answer, one only needs to look to the strategies of the successful European banks and the policy the Japanese government underwent in the late \’90s to eradicate the outbreak.

Firstly, inspiration should be drawn by the change of direction of the Japanese Ministry of Finance. After it became apparent Hougachou alone could not solve the zombie outbreak as zombie banks had no incentive to clean their balance sheets (call in the bad debts). To overcome this an independent Financial Supervisory Agency (FSA) was introduced. The regulator then started to force banks to write down the value of their NPLs, which meant they had to declare insolvency. The independence is the fundamental factor here, as the Ministry of Finance had a vested interest not to expose the high % of NPLs when recapitalizing these banks due to its financial stake. An independent regulator can kill off the zombies rather than keep them alive despite their inability to make a profit. The aggression of the independent regulator in turn forced the Japanese government bodies to reassess how they assisted struggling banks. Rather than simply provide capital to non-viable banks, a significantly larger public fund was set up of 25 trillion yen for recapitalisation. But rather than looking for a ‘quick fix’ with private sector buyers, a new focus was placed on cleaning up the balance sheets of struggling banks. The government set up a public asset management company to acquire and manage NPLs, this provided additional capital to struggling banks and relieved them of the need to manage some of their NPLs. The FSA also introduced financial incentives to improve profitability, which reinforced the need to clean up balance sheets. The combination of the government policy and independent regulations led to drastic reversal in the zombification of Japan’s banking system, as highlighted in the graph bellow.

Source: https://www.ceicdata.com/en/indicator/japan/non-performing-loans-ratio

Equally, there are many banks in Europe which are not struggling, and this is a direct result of their strategy and management. A focus on cost cutting efficiency and embracing digitisation would result in an efficiency drive and in turn start wiping out the infection. The growth of fintech in particular presents an unparalleled opportunity to increase the efficiency of these banks, as there is less and less demand for physical branches, which can significantly reduce overheads. The digital arm of ING (no physical branches) is a fantastic example of the result of embracing digitisation can have, which now boasts a return on equity of 20%. Other successful banks include Santander (ROE 6.37%) and BBVA (ROE 9.78%) both of which have heavily cut costs, invested into technology and relied less on interest rate income risks.

To conclude, an aggressive independent regulator would incentivise zombie banks to self-administer a cure by cleaning up their own balance sheets and force a change to the way governments\’ undergo recapitalization to focus on long-term profitability. This, combined with a change of an individual bank\’s strategic direction, in particular by adopting an innovative fintech strategy, would result in significant increases in efficiency and put to rest the horde sweeping across Europe.

Oliver is a member of TCLA’s writing team. He is a recent law graduate from the University of Nottingham.