Big Commercial Stories | November 2018

UK Digital Services Tax:

The UK has proposed to introduce a 2% digital services tax in April 2020. This would be levied on UK-generated revenues of “specific digital business models”, like search engines, social media platforms and online marketplaces, with global revenues of at least £500m.

This tax aims to ensure that large technology companies pay their “fair share” of taxes on the profits made from services which are provided to users in the UK. This can level the playing field between them and companies that are geographically bound and hence, have been paying a proportionately higher amount of tax.

The UK is now seeking feedback on the design and implementation of this tax ahead of its inclusion in the 2019-20 Finance Bill.

Impact on businesses and law firms:

There are concerns that, even with the minimum revenue threshold, the digital services tax could still unnecessary burden smaller technology companies. Also, given the extent of digitalisation of many businesses, it can be unclear which companies should be considered as entities which are subject to this tax.

Furthermore, as this tax could be seen as discriminatory against large technology companies like Google and Facebook, it could trigger retaliatory measures from the US, where many of these companies are based.

To ensure compliance with the digital services tax, law firms would have to advise their clients on issues like whether they are subject to the digital services tax and how they can structure their operations to minimise the amount of tax they need to pay.

Contributed by: Kit Kuan

Danske Bank Money Laundering:

The story:

Danske Bank, the largest bank in Denmark, has come under fire for the largest money laundering scandal in European history. It is estimated that $234 billion worth of questionable money was circulated in Danske Bank’s Estonian branch from 2007 to 2015.

Danske Bank is currently under criminal investigation by the US Department of Justice for money laundering activities. In 2013, 99% of the Estonian branch’s profits came from non-resident accounts. Many of these were based in Russia, which is currently the subject of US sanctions.

Impact on businesses and law firms:

Businesses breaching money laundering regulations may be subject to massive financial penalties. Just last year, Deutsche Bank was fined $630 million by UK and US authorities for its failure to prevent Russian money laundering activities. Earlier in September, ING Group paid a $900 million penalty for violating Dutch anti-money laundering regulations.

Such businesses may also face significant non-monetary sanctions, such as freezes on dollar funding. In February, the US Treasury accused Latvia’s ABLV Bank of laundering billions of dollars for North Korea’s ballistic missile program, and froze the bank’s dollar accounts. Cut off from the world’s most important market, ABLV subsequently collapsed and was wound up by the European Central Bank.

In addition to direct penalties, businesses associated with money laundering may suffer significant indirect repercussions. For instance, due to shaken investor confidence, Danske Bank’s share price has dropped by more than 30% this year.

The Danske Bank scandal highlights the importance of having active checks on internal anti-money laundering systems. Danske Bank had adopted a three-pronged anti-money laundering strategy, made up of operating guidelines, risk management and internal audit. However, due to the small size of the Estonian branch, Danske Bank did not actively monitor this defence strategy, which ultimately led to its downfall. In May 2018, Denmark’s Financial Services Authority published a report highlighting “deficiencies in all three lines of defence” at Danske Bank’s Estonian branch.

Finally, the EU is facing significant pressure from the US to strengthen its rules on money laundering. Under present rules, the European Central Bank has no independent power to investigate money laundering – it may only do so once a national authority has brought an issue to its attention. However, national regulators in smaller European countries such as Estonia or Latvia may not have the resources or expertise to detect sophisticated financial crime, allowing criminals a window of opportunity. In light of this, several pressure groups have expressed an interest in forming a centralised authority to police money laundering in the EU.

For law firms, the escalation in the global fight against money laundering may present direct opportunities in assisting businesses with drafting internal anti-money laundering policies, or conducting ‘Know Your Customer’ due diligence. Law firms may also be called upon to assist businesses with regulatory compliance and keeping up with their reporting requirements as the regulatory landscape may evolve in the coming years.

Contributed by: Shu Qin Low

US’s Iran Sanctions:

The Story:

In response to Iran’s continued testing of ballistic missiles, on 5th November, Trump reintroduced sanctions that were once removed under the 2015 nuclear deal in exchange for Iran’s cease of nuclear tests. Sanctions imposed on 5th November are part of the second batch of sanctions, with the first batch of sanctions already imposed on August 7th, 2018. This second batch of sanctions is expected to be fatal to Iran’s economy as it targets the core sectors of the economy, from oil exports to banks. The sanctions were re-imposed despite the objections from the UK, Germany, and France, all part of the 2015 nuclear deal.

Impact of businesses and law firms:

What seems important is EU’s response. In a joint statement, the UK, Germany, France, and EU foreign affairs chief Federica Mogherini said that they will protect European companies engaged in legitimate business with Iran, in accordance with EU law. The EU is currently seeking ways to bypass the US sanctions. Some of the methods being discussed include creation of a new European payment system independent of the US-dominated SWIFT, and the use of special purpose vehicle (SPV), which will involve EU member states setting up a legal entity to handle transactions between EU companies and Iran.

These conflicting attitudes of the US and the EU means that lawyers would have to advise companies doing business with Iran on their obligations under US and EU law and how they can mitigate the impact of the sanctions. Law firms would also have to keep abreast of how provisions of US and EU law are being enforced and implemented. Since different firms are affected differently, depending on the industry they are in and their relationship with the US, law firms must make sure that the client’s specific circumstances are considered to accurately capture the impact of the US sanctions.

Contributed by: Sara Moon

UK High Street Retail:

The Story:

High street retail is facing its toughest climate in years. Reports this week state that 14 shops close each day. The autumn budget acknowledged that Brits have embraced internet shopping like almost no other nation. Perhaps its convenience appeals to Brits most as they work some of the longest hours in Europe.

Impact on businesses:

The increased demand for online retail is good for businesses because the costs of selling online are generally 10-20% below high street retailers. However, for high street retailers this means store closures. It is estimated that 40% of the current retail space will become surplus. This will affect property owners because shops won’t need to lease as much space. This lack of demand could decrease property prices and increase the residential property market in high street locations. John Lewis’ new Croydon store only required a 3rd of the space of their traditional stores.

If high street retailers decide to omni-channel (have a combined online and high street presence) they need to manage costs carefully. Store closures will reduce overhead costs but also lose sales from that store. M&S decided to close 100 stores and focus on the most successful parts of the business namely food. Supermarket retail does not seem to be as advanced in terms of online presence vs high street retailers, probably because the process is quite complex and costly, making food deliveries more of a luxury way to shop. PoundWorld, unable to change with the shifting climate, is one of the companies struggling most.

For startups, consumer growth in online retail is great news. They can cut entry costs by going straight online. They also do not have to worry about legacy costs like high street retailers such as high rent, wages and heating. However, low entry costs mean more competition which is why many new fashion lines go under.

Impact on law firms:

An increased demand for restructuring seems inevitable as the high street crisis shows no sign of slowing. Loss of profit will mean high street businesses will be unable to pay overheads and other debts owed to creditors and investors. This may particularly affect privately-owned businesses like Toys R Us which tend to have a lot of debt on their balance sheet. As the high street adapts legal assistance with takeovers and mergers will increase for example House of Fraser and more recently Sainsbury’s. An increasing need for property lawyers is also likely to deal with tenants unable to pay leases and a shift in the property market from retail to residential.

The demand for competition law could rise if the high street were to deteriorate to such an extent that online retailers lacked competition. Although, reliable surveys show demand for high street retail will continue but to a lesser extent so the loss of the high street as a competitor all together seems very unlikely.

Contributed by: Flora Raine

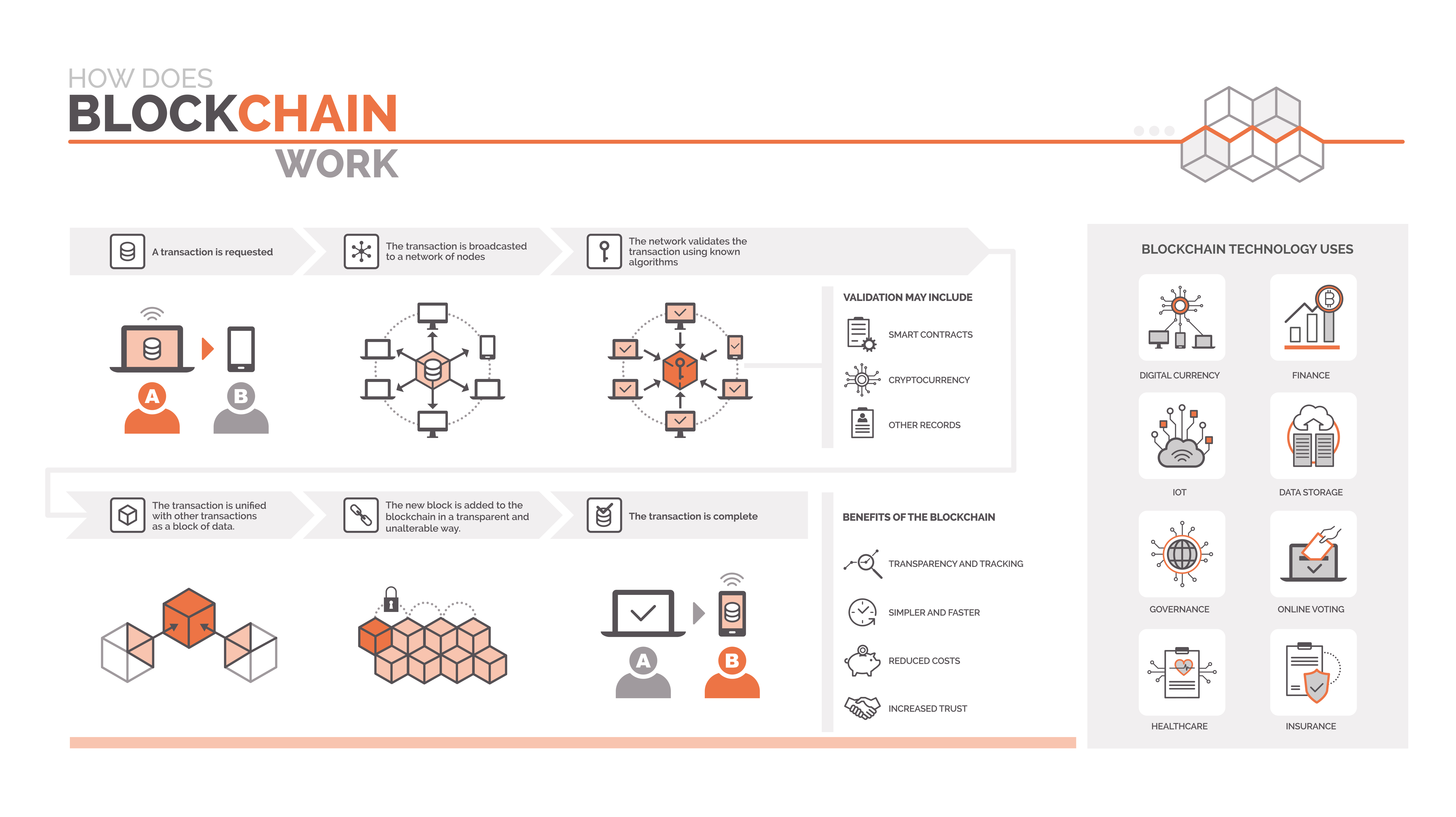

Smart Contracts:

The Story:

Adding to the list of technological advancements in today’s commercial landscape are smart contracts. These are automated contracts that use blockchain technology to log and execute transactions without the need for any human intervention.

Just this week, Change Healthcare made an announcement to collaborate with software provider company, TIBCO, to create a smart contract system to automate healthcare technology. Change Healthcare is a US-based conglomerate that primarily operates as an information exchange intermediary to connect providers, patients and payers in the US healthcare industry. This would allow personal health records to be encoded and stored on the blockchain with a private key to grant access to specific individuals. Other data such as surgery receipts, testing results, drug prescription… etc, could be stored on the ledger and be sent to the relevant parties as such insurance providers.

Indeed, this isn’t breaking news nor is it surprising to anyone anymore. However, it does show how technology is leveraging itself across many industries. With the advantages of smart contracts (see below), it will likely not be long before other sectors, such as the government or those in the management industry adopt this automation.

Impact on businesses and law firms:

To businesses, smart contracts have the potential to increase commercial efficiency by reducing transactional costs such as legal and administrative fees to draft a contract. It provides autonomy by reducing the need for intermediaries to create the contract, it is quick because it reduces the time needed for paperwork, and it is safe since the encryption of data prevents hacking.

Now, this can either be an opportunity law firms to burgeon in the tech sector, or it could be a risk, towards the unprepared, to lose their competitive advantage in the industry especially when clients are so heavily invested in this area today.

To the former, lawyers will be in market to deal with the enforceability of smart contracts, in cases of a breach of smart contracts, because there will be uncertainty as to whether traditional contractual principles (requirements of offer, acceptance, consideration, intention and privity) applies to smart contracts. If they don’t, what will?

Contributed by: Angel Siah

Snapchat Regulatory Investigations:

The story:

Snap Inc., the parent company of the social media platform Snapchat, is facing investigations from the US Securities and Exchange Commission and Department of Justice about the disclosures which Snap made to investors ahead of its initial public offering (IPO) in March 2017.

Snap believes that these regulatory investigations are concerned with the issues raised in a class action lawsuit which investors have filed against Snap in May 2017. The investors in this case claimed that Snap had misled prospective investors about the state of its business. In particular, Snap had allegedly failed to disclose the extent to which competition from Instagram had affected its growth in the second half of 2016.

Impact on businesses and law firms:

Businesses should be aware of the fast-paced rate of technological change and the associated level of market competition that they need to face, as well as take steps to respond accordingly. Aside from it being a matter of strategic concern to keep up with or outdo one’s competitors, this is also a financial issue about ensuring investors’ confidence and hence, the amount of funding which businesses can receive from them.

To ascertain the type and extent of information deemed adequate for the purposes of IPO disclosure, law firms would have to closely monitor the development of this case. This is especially so as, in its pre-IPO S-1 filing, Snap had already stated that it was facing “significant competition” in its business and cited the example of Instagram introducing a feature which “may be directly competitive” with its own Stories feature.

Law firms can then advise their clients who plan to file IPOs and help them to avoid the kind of lawsuits and regulatory investigations which Snap is facing, as well as the proceedings which might arise from the investigations. Even if a law firm’s clients do not plan to file IPOs in the US, given the US’s importance in the global securities market, the standard of IPO disclosure established in this matter might be adopted in other countries.

Contributed by: Kit Kuan

Oil Prices:

The story:

Oil prices have seen significant change in the last month. In October prices reached a four-year high following US sanctions on oil-rich Iran, affecting their exports. This led investors to believe large amounts of oil would disappear from the market causing shortages. However, Russian, Saudi, and US oil companies supply overcompensated for this and Iran’s biggest customers were spared the US sanctions. The oil cartel OPEC also reduced its forecast for global oil demand for next year. This sudden increase and fear of excess supply led prices to fall by over 20%, putting oil into bear market territory. The decrease in price is thought to stabilise as OPEC and Saudi Arabia have spoken about lowering their production for next month.

Impact on businesses:

The price of oil has a far-reaching impact, it affects oil suppliers like BP and Shell, and companies using plastics made from oil, such as Adidas. When oil prices go up too much (around $100 per barrel) it weighs on the consumer, especially in countries like the US where the price feeds into petrol prices quickly and directly. It impacts the cost at the pumps and consumers tend to spend less especially when we know inflation is relatively high and economies like the US and UK rely on buoyant consumer spending. Therefore, such a large drop in price has global economic significance.

A fast decrease in oil price usually worries investors as it signals turbulent times in the world economy and a decline in economic optimism. However, it seems over supply is the cause here. This is good news for consumers and the economy because industries should face less pressure to raise prices, as one of their costs is much lower, leading more money to be spent on other things.

Such a dramatic fall could lift pressures on central banks to curb inflation. America’s central bank will have to rethink its forecast for inflation and reconsider some of its planned interest rate rises. If fuel costs aren’t rising and the Federal Reserve isn’t pushing for higher rates, the pressure will be off of the Bank of England, the European Central Bank and the Bank of Japan to follow suit. Fewer interest rate rises over the next 2-3 years will bring down projected borrowing costs, triggering collective relief from a growing number of indebted companies and consumers across the globe.

It will be interesting see how our consumption patterns change over the next few decades. Oil use for cars is said to peak within the next 7 years as we move towards electric cars. The International Energy Agency’s forecast future growth in oil, even in a decarbonised economy (where our energy is not through oil and gas) because oil is a feedstock to make plastics. This seems quite optimistic considering consumer backlash against single use plastics and countries around the world are likely to take legal steps to reduce plastic.

Contributed by: Flora Raine

M&A deals in the Software Sector:

The story:

On the 11th of November, the $124 billion German software company SAP announced that it is acquiring a US survey software Qualtrics for $8 billion cash. The acquisition is thought to develop SAP’s cloud customer relations business through more sophisticated data collecting that will provide better analysis of customer behavior and response. Five days later, on the 16th, BlackBerry said that it will acquire a cybersecurity firm Cylance for $1.4 billion in cash. BlackBerry, a firm that many people associates with phones, shifted its business to producing cybersecurity software after deciding to stop manufacturing phones in-house in 2016.

These recent deals follow the current trend in the tech sector, where technology giants are snapping up juicy targets to stay ahead in the race. The most popular sector for M&A deals is, according to PWC’s report in October, software; 250 deals were announced last quarter, valuing at up to $41.9 billion. IBM’s acquisition of Red Hat and Microsoft’s acquisition of GitHub were also part of the trend. Big software companies are keen to proceed acquisitions to outrun the looming shadows of fast-growing startups, especially in the cloud-computing business.

Impact on law firms:

Big M&A deals are one of the cash cows of law firms. Lawyers are involved in the entire process: negotiating the deal, carrying out due diligence, and drafting the terms and conditions of the deal. Therefore, the current explosion of tech M&A transactions mean that there are growing number of deals that lawyers can get involved in.

Contributed by: Sara Moon

Criminal Charges against Goldman Sachs:

The story:

On November 1st, charges of money laundering and bribery were filed against Wall Street bank, Goldman Sachs, for their work for a state-investment fund based in Malaysia, 1Malaysia Development Berhad (1MDB). Goldman’s role in this money-tracing maze since 2015 was to underwrite three bond offerings for 1MDB, amounting to a value of $6.5billion, from which it legitimately earned about $600million. However, the US Justice Department claims that the conspirators misappropriated $4.5 billion from the 1MDB fund. This raises the question of whether those involved in the deal (including Goldman) were aware of the integrity of the deals and if so, when. Tim Leissner, Goldman’s former chairman for South-East Asia, had since pleaded guilty to the charges and is due to be sentenced next month.

Impact on businesses:

These unprecedented legal allegations pull Goldman into a regulatory entanglement. The bank could face large fines or be compelled to forfeit the money it made from the bond deals. Taken to the greatest extent, they could be indicted and have its banking charter revoked, although, specialists in money laundering (including Stefan Casella, a former US prosecutor) says that the government is unlikely to go that far.

Nevertheless, investors’ confidence is definitely affected. Since the news broke out, the bank’s shares dipped to their lowest point this week since 2011. Finally, as a bank that prides itself as a high global-standard setter, these allegations risk tarnishing its reputation in the market.

Impact on law firms:

Instead of focusing what law firms can do as a business to fend off money laundering (@Abstruser wrote a great summary on that in the previous commercial law update for the Danske Bank money laundering case), I thought I’ll focus on what law firms can do to help clients fend off this increasingly popular crime.

One precautionary step that lawyers may consider advising their clients to take is review the adequacy of the business’s internal legal and compliance controls. Lawyers may also help their clients evaluate if there is a need to change or enhance the transparency of their clients’ business culture or management through publications.

Contributed by: Angel Siah

The Brexit Withdrawal Agreement:

The story:

The political timeline

In a significant milestone, the UK and EU agreed the text of a draft Brexit agreement last Tuesday. The next day, Prime Minister Theresa May secured the support of her cabinet ministers after a five-hour emergency meeting. While the cabinet reached a collective decision, it was not unanimous – 11 members objected to the deal, with 18 supporting it. Work and pensions secretary Esther McVey and Brexit secretary Dominic Raab resigned from cabinet the following morning. Following this, Donald Tusk announced that an EU summit will be held on November 25, 2018 to finalise the provisional Brexit deal.

Still, the hurdles are far from over. After the summit, the EU Withdrawal Act 2018 requires the final text to be approved by an ordinary resolution of the House of Commons. Theresa May will need 320 votes to approve the withdrawal agreement, but the Conservatives have only 318 MPs in Parliament. Internal dissent from Conservative hard Brexiters (such as Jacob Rees-Mogg) and Remainers (such as Dominic Grieve) further threatens the Prime Minister’s ability to gather the necessary votes to cement the deal.

Growing unrest surrounding Theresa May’s premiership may further complicate matters, as a number of Conservative MPs have moved to trigger a vote of no confidence against her. A motion of no confidence is triggered when 15% of Conservative MPs (48 members) submit letters of no confidence to the chairman of the 1922 Committee. 25 MPs have publicly stated they have submitted such letters, but the total number may well exceed this. Should Theresa May be toppled as Prime Minister, it could severely delay the finalisation of the withdrawal agreement, increasing the risk of a no-deal Brexit.

The withdrawal text

Under the provisional deal, a 21-month transitional period will run from March 29, 2019 to December 31, 2020 during which all EU legislation “shall be binding on and in the United Kingdom”. This period is designed to allow the EU and UK to conclude a future trade agreement. This transition period may be extended, but any extension would be subject to further contributions to the EU common budget.

On financial contribution, the draft agreement requires the UK to honour all financial commitments to the EU as if it were still a member for the years 2019 and 2020. The UK Treasury estimates this ‘exit bill’ to amount to €40-45 billion, though by some estimates the figure is closer to €60 billion.

Crucially, until a future trade deal is agreed, the UK (including Northern Ireland) shall be the part of a temporary ‘backstop’ customs union with the EU. As long as the backstop remains in place, the UK shall commit to a “level playing field”, following EU competition rules and maintaining close alignment with labour, tax and environmental laws.

As to Northern Ireland, a hard border will be avoided and goods may be freely circulated across the island of Ireland. Checks on trade will instead take place within the UK mainland. However, the price to pay is steep – Northern Ireland will be bound by the EU’s customs and single market rules, thereby remaining in a much closer customs relationship with the EU than the rest of the UK.

Impact on businesses:

Businesses and investors alike will continue to keep a close eye on Brexit, as the pound continues to fluctuate as Brexit unfolds. The volatility of the pound has calmed somewhat, pending presentation of the draft withdrawal text before the House of Commons, but it is still trading 14% lower than on the referendum day. Analysts at Societe Generale and JPMorgan predict that the pound will benefit if a deal is accepted by Parliament, which will offset inflation as well as buoy wages and consumer spending. However, in the event of a no-deal Brexit, Standard & Poor estimates that the pound could fall a further 15% against the US dollar.

For companies planning their business operations, the withdrawal text presents a clear, if not altogether ideal, starting point from which to map future developments and possibilities. Three clear scenarios appear: no-deal, transition, and backstop.

Scenario 1: No-deal

If the withdrawal agreement is not accepted by Parliament, the chances of no-deal Brexit become alarmingly high. The EU has made it clear that the terms of withdrawal are more or less final, with Angela Merkel stating that “[t]he question of further negotiations does not arise at all”. If the UK fails to sign a formal treaty with the EU by early December, UK officials have stated that contingency plans for a no-deal Brexit will have to be triggered.

Without a withdrawal agreement, the UK would default to WTO trade rules on March 29, 2019, which would require the imposition of tariffs and checks at the UK border – including the Northern Ireland border. This would severely impact businesses and their supply chains. Health Secretary Matthew Hancock warned that deaths could result from medicine shortages in the event of a no-deal Brexit.

Scenario 2: Transition period

If the withdrawal agreement does pass through the House of Commons, businesses will be briefly comforted by the short-term certainty provided by the transition period. It should be noted that the draft text covers only withdrawal arrangements. The future UK-EU trade relationship will be subject to further negotiations once the UK has exited the EU. For businesses, this means that plans may safely be made up until the end of 2020, but long-term certainty will depend on the future trade relationship negotiated after Brexit.

Scenario 3: The ‘backstop’

If no trade agreement is reached by the end of 2020, the backstop regime will kick in. Even this possibility is worrying, as the threadbare backstop omits several arrangements crucial to business operations. These omissions are wholly intentional – Sabine Weyand, the EU’s deputy chief negotiator, has stated that the backstop was designed to ensure the UK could not rely on it indefinitely, giving the EU greater bargaining power in negotiations for the future trade agreement.

For example, the backstop does not include an agreement on road transport. British drivers will need to apply for new international licenses and regulatory certificates to travel in Europe, a time-consuming and bureaucratic process. The backstop also does not commit the UK to regulatory alignment with the EU on goods, which will likely lead to extensive product standard checks on goods crossing UK borders.

For UK financial services, the backstop only contemplates a basic level of access to EU financial markets based on the principle of equivalence. Equivalence assessments would commence as soon as possible after Brexit, with the aim of being concluded before the end of 2020. The EU currently grants equivalence to several other countries, such as Singapore and the US. However, the problem with the equivalence regime is that it largely focuses on wholesale activities such as securities trading. There is no such regime for retail activities such as commercial lending and insurance, which will affect British retail banks and insurers if a future trade agreement is not secured. This is likely to prompt more British financial institutions to set up shop in the EU in order to retain existing customers.

Impact on law firms:

Similar to businesses, the draft text allows law firms to begin analysing industry-specific implications of each Brexit scenario in order to advise clients accordingly. Many law firms have already begun this process – Simmons & Simmons, for instance, launched its Disputes Aviator tool to help clients conceptualise the impact of various Brexit scenarios on English jurisdiction and governing law clauses in future and existing contracts.

Law firms themselves may also begin consolidating their strategies for each possible scenario. For example, to prepare for a no-deal Brexit, Freshfields, Slaughter and May, and Eversheds Sutherland have registered several of their lawyers to the Irish Roll of Solicitors in order to retain rights of audience before the CJEU and professional privilege in regulatory probes by the European Commission. Similarly, Simmons & Simmons, Covington & Burling and Pinsent Masons announced their intentions to launch offices in Dublin following the Brexit vote.

Contributed by: Shu Qin Low

Google’s Absorption of DeepMind:

The story:

Alphabet, Google’s parent company, would be absorbing DeepMind Health, the medical unit of DeepMind, which is a UK Artificial Intelligence (AI) company owned by Alphabet, into the newly formed, US-based Google Health.

As part of its current work with certain NHS hospitals, DeepMind Health has access to the medical records of 1.6 million NHS patients. DeepMind has stated that, post-business consolidation, the data remains under the control of its NHS partners and that “its processing remains subject to both [DeepMind’s] contracts and data protection legislation”. Still, this planned absorption has raised privacy concerns that Google can incorporate the data in such records into Google’s products or services without the patients’ consent.

Impact on businesses and law firms:

As data is becoming an increasingly valuable asset, there will be greater awareness and hence, scrutiny of commercial entities’ potential non-compliance with data protection rules. This is especially so given the rise of stringent regulations like the General Data Protection Regulation (GDPR), as well as the recent high-profile data breaches such as the one involving British Airways.

Even if businesses are not directly collecting or using data in fairly innocuous and common commercial dealings, they need to be alert to the wider data protection implications that can arise from such dealings. Law firms are more likely to have to handle matters like helping their clients to structure their operations, negotiate their deals and draft their agreements with prospective clients and business partners more tightly, with a view to pre-empting possible data protection-related problems.

Contributed by: Kit Kuan

Impact of a no-deal Brexit on Businesses and Law Firms:

1. An optimistic future

Without a deal with the EU, Brexiteers would hope for the UK to prosper outside the EU and that this would be a way of avoiding paying the divorce settlement to Brussels.

If a no-deal Brexit kicks in, it is likely that the UK would trade with the EU on standard terms used by members of the World Trade Organisation. These terms will not be as favourable to the UK as an outsider than they would be to the EU’s members simply because the UK’s exports to the EU would now be subjected to tariffs. However, the optimism is that the UK will eventually get used to this. While it will be a painful process, the hope is that the opportunity for the UK to trade independently with the rest of the world balances out the losses.

2. The realistically less optimistic future

However, the more realistic result is that a no-deal Brexit risks a very bad deal. With 45 years of arrangements intertwined between the EU and the UK, the UK’s relationship with the EU goes way beyond a trade deal. The UK’s membership of the EU’s single market (a customs union that many businesses benefit from) would cease. Without a deal, there will be grave uncertainty as to the costs that businesses will have to face once the privilege to trade freely is taken away.

no-deal Brexit would leave the UK without rules to govern crucial matters such as immigration control, aviation, medicines regulation and financial transactions. Again, this would be a time when many businesses would seek legal advice for contingency plans.

It is true that the Remainers’ forecast for the UK to go into a recession post-Brexit did not come true. However, the performance of the UK’s economy has not been the best either. It has declined compared to other advanced economies. From being the fastest growing member of the G7, the UK is now one of the slowest. While this may be attributed to external economic factors, such as a slower global economy, one cannot deny that the uncertainty of the UK politics in recent years has hampered investors’ confidence. A no-deal Brexit may have even more profound effects.

Finally, a situation that businesses and law firms may want to prepare for is the possibility for a major political change in the future, including a potential change of government. Since the agreement took place, not only have a number of high-profile ministers resigned from office but an ever-growing number of MPs have submitted letters of no confidence on Mrs May as well. As a matter of background, a vote of no confidence is a vote by the PM’s own MPs against her to be deemed as no longer fit to hold her office. For the vote to succeed, a total of 48 Tory MP’s vote is required. To date, approximately 25 votes has been obtained. If Mrs May wins the confidence vote, she will remain in office and awarded immunity for a year. If she loses the vote, she will have to resign.

Contributed by: Angel Siah

The US Tech Stock Sell-off:

The story:

US stocks have experienced extreme volatility over the past two months. The S&P 500 and tech-heavy NASDAQ ended October 6.9% and 11% down, making it the indices’ worst performing month since 2009. Investors seeking to ‘buy the dip’ were wrongfooted, as the stock sell-off continued well into November. Tech stocks were particularly hard hit. The sell-off has seen more than $1 trillion worth of market value wiped off from the big five ‘FAANG’ technology companies. Last Tuesday, Apple fell 3.9%, Facebook dropped 3.4%, Netflix declined by 5%, Amazon dropped 4.4% and Google parent Alphabet fell 2.3%.

There are many factors driving the broader market sell-off, but a key reason is the US Federal Reserve’s quantitative tightening policy, under which interest rates have risen three times this year. As interest rates rise, the cost of borrowing is expected to put pressure on American companies. The fear of a global economic slowdown helps to explain the recent tech sell-off, as investors move from speculative internet and tech stocks towards safer stocks such as real estate and utilities. The US-China trade dispute may also be affecting recent sentiment towards tech companies, as many of them rely on Chinese manufacturers and chipmakers.

However, some of the tech stock woes aren’t directly tied to the trade war or rising interest rates. Facebook, for instance, has come under recent fire for admitting that it hired research and public affairs companies to investigate and discredit George Soros, a well-known critic of the company’s business model. Users leaving Facebook, and the threat of litigation against the company have led investors to be wary of the future of the company. Apple, as well, has been having difficulty expanding their customer base, and recently slowed production for many of their new iPhone models. Apple will now stop announcing how many units they sold per quarter to the stock holders, which has prompted many investors to flee.

Impact on businesses and law firms:

For many listed companies, the sell-off presents a threat as investor fear begins leaking into other sectors and regions outside of the US tech market. Poor performance from the FAANG companies, which have led the global stock market for over a decade, has sparked investor fear that the longest bull-market in history has come to an end. Morgan Stanley, for instance, has begun warning customers that the stock sell-off indicates the beginning of a bear market. Additionally, with both the US Fed and the ECB moving towards a regime of quantitative tightening, higher interest rates are beginning to make bonds seem more attractive than stocks.

The recent stock sell-off may also impact business funding models. For instance, venture capital, which drives many tech startups, may not be as easily accessible, as investors move towards more defensive instruments like bonds or consumer staple stocks. As such, companies may seek to re-evaluate their business funding options, which creates opportunities for law firms to advise on debt restructuring and broader financing.

Contributed by: Shu Qin Low

Fall of the Pound 2016 – 2018:

The story:

Many factors determine a currency’s rise and fall but for the pound Brexit is way ahead of other causes. The market hates uncertainty and as there was little knowledge of what Brexit really meant for the UK economy traders instincts leaned towards selling the pound. This caused the pound to fall around 11% following the referendum.

The future value of the pound will be determined by the political outcome around Brexit in the next couple of years. US Investment Bank, Goldman Sachs believes the pound will rally vigorously next year against the euro and the US dollar. They forecast an increase of 4.6% and 10% from current levels to 1.176 euros and 1.41 dollars, as long as the UK shifts into a “status-quo” transition on Brexit day.

Impact on business:

A weaker pound benefits many FTSE 100 and FTSE 250 companies as their earnings tend to come from abroad. Therefore, a stronger pound impacts the larger more international company’s earnings, dividends and ultimately their value. The more domestically orientated mid-sized 250 index (a more diverse group of companies that better reflects the UK economy) benefit slightly less. However, compared to US companies and other peers, UK companies are underperforming in the long term.

The value of the pound and share prices are thus linked (when the pound goes up shares go down and vice versa). That relationship is going to continue to hold because three-quarters of revenues from the largest 100 companies are earned from outside of the UK.

Impact on law firms:

London’s biggest law firms have benefited from a weaker pound due to their overseas growth. A study by PwC found that foreign exchange movements contributed around two-thirds of overall fee income growth and almost half of profit growth in the UK’s global top ten firms. Their financial results are being propped up by earnings from their array of international offices which are then boosted when converted into pounds at the current favourable exchange rates. Allen & Overy said almost three-quarters of its 2016 revenue came from issues involving two or more countries. PwC estimates the weak pound is contributing an average of £43.7 million of revenue and £16.2 million of profit to the top ten firms.

Contributed by: Flora Raine

Accounting Firms’ Disruptions in the Legal Service Sector:

The story:

According to Legal Cheek’s article published last Friday, KPMG, one of the ‘Big Four’ accounting firms in the world, announced that it will increase the number of its lawyers to over 3,000 in the next few years. If it reaches this ambitious target, then it will become one of the largest ‘law firms’ in the world. Considering that Denton, the current largest law firm in the world, has over 9,000 lawyers and Linklaters and Allen & Overy, both part of the magic circle, have 2,100 and 2,800 lawyers respectively, KPMG’s target headcount forewarns traditional law firms of the possible—or even already initiated—upheaval in the legal sector.

KPMG’s announcement is just one of the numerous changes accounting firms have been making in their business over the last few years to infiltrate the legal industry. EY, for example, acquired Riverview Law, a legal service firm, this September as part of their project to expand the global legal managed services. PwC currently has over 3,500 lawyers in 90 countries and its UK branch offers legal services in 13 different areas. It also opened a law firm, ILC Legal, in Washington DC last year. Deloitte’s legal network, which includes over 2,400 lawyers in over 80 countries, recently saw another local Singaporean law firm, Sabara Law, added to it. Some of these firms—KPMG and PwC—also offer training contracts (while EY used to offer training contracts, it announced that it has no plan to do so in the current cycle).

These threatening business transformations of Big Four accounting firms could be said to be driven by their client needs and profitability. Many clients prefer to seek legal advices from the firm they obtain non-legal services because this leads to integration of, and thus more effective provision of, legal and non-legal services in certain corporate or commercial transactions. At the same time, ability to provide legal advices, especially in the areas of tax and corporate, can make these firms highly competitive because these are not something that traditional accountants offer.

Impact on businesses and law firms:

To businesses, disruption caused by big accounting firms in the legal market is good news. These firms will drive up competitions in the legal market, which is likely to lead to lower cost to clients. Downward trend in legal service cost is especially likely considering that the Big Four are investing hugely in technology in order to innovate their legal services and provide clients with more cost-effective solutions. Also, clients can enjoy benefits arising from the Big Four’s globally wide community of experts and strong consulting advisory capability when seeking legal advices from these firms.

However, rise of the Big Four in the legal market is a nightmare to traditional law firms. According to a survey conducted by ALM Intelligence last year, 69% of law firms said that they see Big Four as their biggest competitors, more than the in-house law departments. Concerns shown by law firms are understandable because accounting firms already possess strong base to establish new legal service businesses and are effectively using them to compete existing law firms; they are already renowned professionals in the areas of tax, finance and M&A and are focusing on these areas of law to complement and strengthen their existing non-legal services provided to their existing wide client base. Law firms must develop strategies to survive the threat posed to their market shares and revenue by the Big Four.

Some of the law firms are already preparing for the looming transformation of the legal market. For example, Allen&Overy surprised the consulting market by launching its own regulatory consultancy this summer, showing that Big Four’s disruption in the legal market is not a one-way attack. In addition to this, many of the law firms are joining the technology race by innovating their legal services to become more efficient and less costly. In regard to tax, law firms are not just advising on law but also other aspects of tax planning, such as financial and economic aspects to compete with accounting firms. Baker & McKenzie, for example, hired Mark Bevington, a former partner at EY and half of its corporate tax team consist of non-lawyers. As shown by these moves, in order to maintain competency in the market, traditional law firms would have to constantly develop their services to survive the increasing competition caused by the accounting firms.

Contributed by: Sara Moon

accordion

interview-questions